United Kingdom Loyalty Business Report 2026: A $4.06 Billion Market by 2030 from $2.33 Billion in 2025

Table of Contents

Company Logo

The UK loyalty market presents key opportunities by evolving beyond “points” to personalized, app-led models integrated into daily shopping, emphasizing frictionless digital experiences. Expanding into financial services enhances retention, while partnerships increase ecosystem value, maintaining compliance in a competitive landscape.

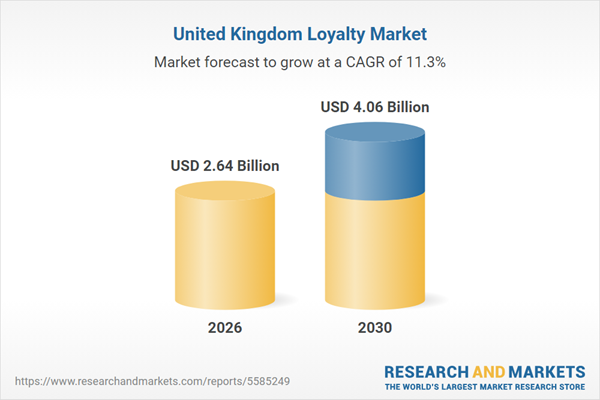

The loyalty market in United Kingdom is expected to grow by 13.5% annually, reaching US$2.64 billion by 2026. The loyalty market in the country has experienced robust growth during 2021-2025, achieving a CAGR of 15.5%. This upward trajectory is expected to continue, with the market forecast to grow at a CAGR of 11.3% from 2026 to 2030. By the end of 2030, the loyalty market is projected to expand from its 2025 value of US$2.33 billion to approximately US$4.06 billion.

The UK loyalty program market is characterised by high penetration, strong incumbents, and competition driven by continuous refinement rather than disruption. Scale players anchor the market through everyday relevance, while technology providers compete to become critical infrastructure partners. Over the forecasting period, competitive dynamics are expected to be shaped by the ability to integrate loyalty deeply into commercial operations, extend value through controlled partnerships, and operate within a tightening regulatory environment.

Competition is centred on optimisation rather than program creation

The UK loyalty market is structurally mature, with high consumer participation across retail, travel, and financial services. Competitive intensity is therefore driven by continuous optimisation of existing programs rather than new scheme launches. Large brands are refining mechanics, benefit structures, and digital journeys to protect engagement and relevance, while avoiding disruption to established member bases. As a result, competitive differentiation increasingly sits in execution quality how loyalty is embedded into pricing, checkout, and customer communications rather than in headline rewards.

Scale players dominate member relationships, limiting displacement risk

The competitive landscape is anchored by large, high-frequency operators. In grocery and retail, players such as Tesco, Sainsbury’s, and Marks & Spencer use loyalty as a core commercial lever tied closely to pricing and promotions. In travel, British Airways continues to set expectations for coalition-style loyalty through Avios. These programs benefit from scale, data depth, and habitual usage, making competitive displacement unlikely. However, their size also means innovation is typically incremental rather than radical.

Key trends and drivers shaping the UK loyalty program market

Across the UK, loyalty is evolving from a “card-and-points” construct into an app-led, personalised and partnership-driven capability that sits inside everyday shopping and service relationships. In the forecasting period, the programs that win share of attention are likely to be those that combine targeted value in core categories, frictionless digital membership, and partner breadth while meeting rising expectations for transparency and compliant customer journeys.

Shift loyalty from “points” to personalised value in essential categories

Major UK grocers are pushing loyalty into more tailored, mission-led mechanics rather than relying only on generic points accrual. Tesco’s 2025 initiative tied Clubcard rewards to fruit and veg with personalised rewards mechanics, signalling a move toward targeted offers that are easier for households to notice in-day-to-day shopping.

The UK consumer environment remains cost- and value-sensitive, and supermarkets are using loyalty as a primary lever to influence basket choices and trip frequency without relying solely on broad promotions. This also aligns with retailers’ need to defend share in a highly substitutable grocery market where switching costs are low.

Expect retailers to deepen “value-plus-personalisation” models more targeted challenges, category missions, and tailored rewards because it lets them defend price perception while controlling margin impact more tightly than across-the-board discounting.

Make the loyalty app the primary operating system for membership

UK loyalty is increasingly being rebuilt around app-led membership experiences. Central Co-op, working with Lobyco, launched a new membership app and positioned it as the core member experience, including cashback-style benefits, gamified features, and personalised promotions

UK retailers want lower-friction identification at checkout, tighter linkage to first-party customer data, and more direct control over member communications especially as traditional third-party targeting faces constraints. App adoption also enables faster iteration of mechanics (missions, rewards, partner offers) than plastic-card-only programs.

App-led programs will become the default design pattern in the UK beyond the largest grocers, with mid-sized retailers and member-owned groups modernising legacy propositions. This raises the bar for usability, digital identity, and real-time offer delivery.

Extend loyalty beyond retail into financial services “rewards-as-a-product”

UK banks are increasingly packaging loyalty as a formal account feature to defend primary banking relationships often using travel or everyday rewards constructs. Barclays positions Avios earning as part of its Premier proposition, framing loyalty as a retention and engagement tool embedded in the banking relationship.

UK consumers hold multiple financial products and can switch providers; banks use rewards to reduce churn and increase product stickiness. This also reflects the broader UK pattern of strong travel-rewards affinity and co-branded ecosystems.

More “bundle economics” is likely loyalty benefits tied to account tiers, subscriptions, or packaged services while banks and partners refine unit economics and eligibility rules to keep reward costs predictable.

Use partnerships to turn loyalty into an ecosystem rather than a single-brand benefit

UK loyalty programs are leaning further into partnerships that deliver non-transactional access and experiences, not just discounts. British Airways, for example, announced a partnership positioned around exclusive benefits for loyalty members with Olympia.

UK consumers are already members of multiple schemes; partnerships let brands add perceived breadth without building everything in-house. For operators, partnerships can widen earning/burning options and create reasons to engage outside the core purchase cycle.

Expect more cross-sector collaborations (travel-events, retail-services, payments-rewards) and more structured partner governance, because ecosystem value increasingly determines whether a program is used versus merely held.

Tighten compliance around loyalty-linked pricing, fees, and reviews to protect trust

UK consumer protection enforcement is sharpening around price transparency and online practices areas that directly affect loyalty-linked offers, member-only pricing presentation, and digital conversion flows. The Digital Markets, Competition and Consumers Act 2024 is in force, and related guidance/consultation activity in 2025 has focused on clearer price presentation and transparency expectations.

Regulators are targeting consumer harm from unclear pricing and misleading online practices, and loyalty programs often sit directly in the purchase journey (member prices, app-only offers, add-ons, and partner redemptions). Maintaining trust is operationally critical when loyalty becomes more digital and personalised.

UK program owners will invest more in governance how member pricing is messaged, how benefit terms are disclosed, and how reviews/claims are managed across owned and partner channels to reduce regulatory and reputational exposure.

Key Attributes:

Report Attribute

Details

No. of Pages

127

Forecast Period

2026 – 2030

Estimated Market Value (USD) in 2026

$2.64 Billion

Forecasted Market Value (USD) by 2030

$4.06 Billion

Compound Annual Growth Rate

11.3%

Regions Covered

United Kingdom

Report Scope

United Kingdom Retail Sector Market Context

United Kingdom Retail Industry Market Size, 2021-2030

United Kingdom Ecommerce Market Size, 2021-2030

United Kingdom POS Market Size Trend Analysis, 2021-2030

United Kingdom Loyalty Spend Market Size and Growth Dynamics

United Kingdom Loyalty Spend Market Size and Future Growth Dynamics, 2021-2030

United Kingdom Loyalty Spend on Schemes by Value Accumulated and Value Redemption Rate, 2025

United Kingdom Loyalty Spend Share by Functional Domains, 2021-2030

United Kingdom Loyalty Spend by Loyalty Schemes, 2021-2030

United Kingdom Loyalty Spend by Loyalty Platforms, 2021-2030

United Kingdom Loyalty Schemes Spend Segmentation by Loyalty Program Type

Point-based Loyalty Program

Tiered Loyalty Program

Mission-driven Loyalty Program

Spend-based Loyalty Program

Gaming Loyalty Program

Free Perks Loyalty Program

Subscription Loyalty Program

Community Loyalty Program

Refer a Friend Loyalty Program

Paid Loyalty Program

Cashback Loyalty Program

United Kingdom Loyalty Schemes Spend Segmentation by Channel

United Kingdom Loyalty Schemes Spend Segmentation by Business Model

United Kingdom Loyalty Schemes Spend Segmentation by Key Sectors

Retail

Financial Services

Healthcare & Wellness

Restaurants & Food Delivery

Travel & Hospitality (Cabs, Hotels, Airlines)

Telecoms

Media & Entertainment

Other

Sector Channel Views: Loyalty Schemes Spend by Key Sectors and Channels

Online Loyalty Spend by Sector, 2021-2030

In-store Loyalty Spend by Sector, 2021-2030

Mobile App Loyalty Spend by Sector, 2021-2030

United Kingdom Retail Sector Deep-Dive: Loyalty Schemes Spend by Retail Segment

United Kingdom Loyalty Schemes Spend Segmentation by Accessibility

Card Based Access

Digital Access

United Kingdom Loyalty Schemes Spend Segmentation by Consumer Type

B2B Consumers

B2C Consumers

United Kingdom Loyalty Schemes Spend Segmentation by Membership Type

Free

Free + Premium

Premium

United Kingdom Loyalty Spend Split by Embedded vs. Non-Embedded Loyalty

United Kingdom Loyalty Spend Split by Use of AI / Blockchain

United Kingdom Loyalty Platform Spend Segmentation by Software Use Case

Analytics and AI Driven

Management Platform

United Kingdom Loyalty Platform Spend Segmentation by Vendor / Solution Partner

In-house

Third-Party Vendor

United Kingdom Loyalty Platform Spend Segmentation by Deployment

United Kingdom Loyalty Platform Spend Segmentation by Offering

United Kingdom Consumer Demographics & Behaviour (Loyalty Spend Share), 2025

Age Group

Income Level

Gender

United Kingdom Loyalty Program KPIs, Behavioral Metrics & Embedded, 2025

About ResearchAndMarkets.com ResearchAndMarkets.com is the world’s leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood,Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./ CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900

Join millions of self-starters in getting business resources, tips, and inspiring stories in your inbox.

Unsubscribe anytime. By entering your email, you agree to receive marketing emails from BigBCC. By proceeding, you agree to the Terms and Conditions and Privacy Policy.

SELL ANYWHERE WITH BigBCC

Learn on the go. Try BigBCC for free, and explore all the tools you need to start, run, and grow your business.