✅ Silicone Market Outlook: Powered by Innovation, Urbanization & High-Performance Demand

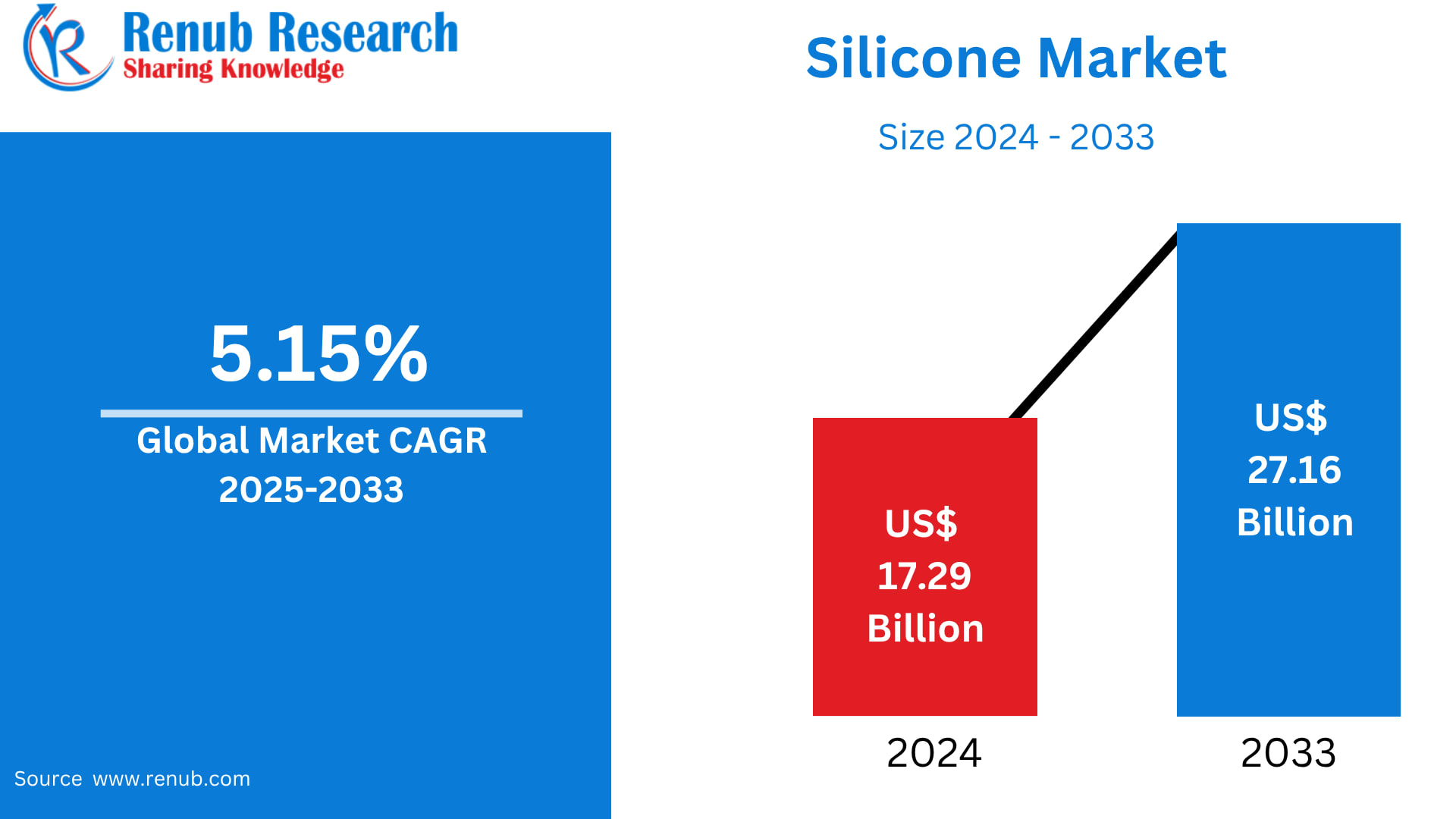

According to Renub Research, the global silicone market was valued at approximately US$ 17.29 billion in 2024. The industry is projected to grow at a 5.15% CAGR between 2025 and 2033, ultimately reaching US$ 27.16 billion by 2033.

This growth underscores silicone’s role as an indispensable industrial material—known for its heat resistance, flexibility, electrical insulation, and biocompatibility. Used across construction, automotive, electronics, medical devices, renewable energy, and personal care, silicone continues to migrate into high-tech and sustainability-driven applications.

Why Silicone Demand Is Accelerating

Urbanization & infrastructure growth increasing use of sealants, coatings, and adhesives

Electronics miniaturization requiring advanced insulating materials

Medical-grade silicones expanding due to implants, wearables, and surgical tools

Electric vehicles & renewable energy requiring silicone in batteries, solar panels, and wind components

High-performance manufacturing demanding chemical and thermal stability

From skyscrapers to pacemakers, silicone has become one of the silent engines powering modern industry.

✅ Top Global Companies in the Silicone Market

Below is a breakdown of major players defining the sector through innovation, capacity expansion, mergers, and sustainability-led strategies.

1. Illinois Tool Works Inc. (United States)

Founded: 1912

Headquarters: Glenview, Illinois

Illinois Tool Works (ITW) is a diversified manufacturer producing adhesives, sealants, chemical fluids, welding systems, and industrial equipment. With customers in automotive, construction, aerospace, foodservice, and industrial production, ITW leverages a decentralized business model and global distribution network.

Key Strengths

Broad product portfolio covering multiple silicone applications

Global presence in U.S., China, France, Germany & U.K.

Strong industrial customer relationships

Strategic Direction

ITW is focusing on specialty chemical growth, high-margin segments, and aftermarket services, positioning silicone solutions as part of its long-term industrial materials strategy.

2. Evonik Industries AG (Germany)

Founded: 2007

Headquarters: Essen, Germany

Evonik is a leading specialty chemicals powerhouse supplying polymers, additives, silicones, and surfactants. Serving sectors from electronics and pharmaceuticals to construction and renewables, Evonik emphasizes sustainability and high-performance chemistry.

Key Advantages

Manufacturing hubs across Germany, Belgium, U.S., China & Singapore

Strong engineering and technical services ecosystem

Diverse market exposure

Evonik is investing heavily in green chemistry, energy-efficient silicones, and material innovations for EV batteries and solar technologies—positioning itself for high-tech market penetration.

3. Kemira Oyj (Finland)

Founded: 1920

Headquarters: Helsinki, Finland

Kemira specializes in chemicals for water-intensive industries, including pulp & paper, oil & gas, mining, and wastewater treatment. Its silicone-based dispersants, polymers, and coatings enable more sustainable industrial processes.

Competitive Strengths

Strong footprint in municipal & industrial water treatment

Advanced process monitoring & specialty chemical services

Growing demand for water-efficiency technologies

As global water concerns rise, Kemira is uniquely positioned to benefit from sustainability-driven silicone adoption.

4. Elkem ASA (Norway)

Founded: 1904

Headquarters: Oslo, Norway

A leader in silicon-based materials, Elkem produces silicones, ferrosilicon, carbon products, and microsilica. Serving industries such as solar energy, automotive, construction, and aluminum, the company integrates advanced R&D with deep manufacturing heritage.

Core Capabilities

Vertically integrated silicon production

Strong presence in renewable energy supply chains

Global expansion backed by Bluestar Elkem International

Elkem’s focus on low-carbon production aligns with rising ESG requirements across global markets.

5. Kaneka Corporation (Japan)

Founded: 1949

Headquarters: Osaka, Japan

Kaneka manufactures PVC products, advanced plastics, life science materials, and silicone solutions. With R&D centers dedicated to biotechnology, regenerative medicine, and material innovation, Kaneka is pushing silicone into next-gen medical and industrial sectors.

Strategic Focus

Advanced materials for electronics and healthcare

Global expansion across Asia, Europe, Africa & the Americas

Cell therapy and biomaterials research

Kaneka’s manufacturing strength and innovation pipeline offer significant market expansion potential.

✅ SWOT Spotlight: Two Emerging Silicone Innovators

Specialty Silicone Products, Inc.

Strength:

Deep expertise in high-performance silicone formulations for aerospace, defense, medical, and electronics. Their materials offer high-temperature resistance, low outgassing, and extreme durability—ideal for mission-critical applications.

Opportunity:

Rapid growth in medical implants, aerospace components, space exploration, and cleanroom electronics creates a premium niche that SSP is well-positioned to dominate.

Gelest, Inc. (Part of Avantor)

Strength:

Strong R&D, backed by Avantor’s global infrastructure, enables Gelest to deliver high-purity silicone materials for electronics, optics, and biomedical applications.

Opportunity:

Explosive demand in semiconductors and biomedical coatings, implants, and drug delivery presents a scalable growth path—especially as chip miniaturization accelerates.

✅ Sustainability Leadership: Dow Inc.

Dow aims to achieve:

Carbon neutrality by 2050

30% emission reduction by 2030

Circular economy initiatives via advanced recycling

Collaborations to eliminate plastic waste

Dow also integrates natural capital and water stewardship into its operating model, strengthening ESG transparency and product innovation. With growing regulatory pressure, Dow’s sustainability strategy positions it as a frontrunner in responsible silicone production.

✅ Recent Developments Reshaping the Silicone Market

May 2025:

Shin-Etsu Chemical launched KF-6070W silicone wax and new elastomer gels for improved sensory performance in personal care.

June 2025:

WACKER introduced POWERSIL 1900 A/B, optimizing silicone rubber for composite insulator manufacturing.

May 2024:

Momentive Performance Materials acquired Elkem ASA’s silicone business, expanding European reach and strengthening its global portfolio.

These developments signal a shift toward:

Specialty silicone materials

Personal care innovations

Power infrastructure applications

Strategic acquisitions for market consolidation

✅ Key Industry Growth Drivers (2025–2033)

Electric vehicles & battery insulation

Semiconductor manufacturing

Wearable health devices

Solar power & wind turbine components

Smart construction materials

Minimally invasive medical devices

Silicone is moving from a commodity chemical to a high-value enabler of futuristic technologies.

✅ Market Risks & Challenges

Raw material price volatility

Environmental regulations & disposal concerns

High capital investment for ultra-pure silicone production

Competition from low-cost manufacturers

Companies prioritizing innovation, clean production, and specialty niches are most likely to thrive.

✅ Final Thoughts: The Silicone Market’s Next Decade

The silicone market is transitioning into a technology-driven, sustainability-focused, and innovation-led era. With demand expected to reach US$ 27.16 billion by 2033, the sector will see major expansion in:

✅ Renewable energy

✅ Advanced electronics

✅ Medical applications

✅ Sustainable infrastructure

Meanwhile, mergers, R&D investments, and circular economy initiatives will reshape competitive dynamics.

In short, silicone isn’t just a material—it’s the backbone of modern manufacturing, future energy systems, and next-generation healthcare.