The processed and frozen vegetables market sees opportunities in automation, sustainable practices, modernized packaging, and diversified sourcing. Companies can enhance supply chain agility, improve compliance, and mitigate risks by adapting to changing regulations and consumer demands.

The processed and frozen vegetables market demonstrates steady growth, with ongoing global demand driving consistent industry advancement. Companies are accelerating automation to streamline internal workflows, boost traceability, and align with evolving sustainability frameworks. Modernized packaging solutions and responsible sourcing methods are increasing in response to changing regulatory standards.

Additionally, businesses are reinforcing logistics networks and adjusting supply chain models to remain agile in the face of consumer and policy shifts. Industry innovation continues to shape operational benchmarks, enabling organizations to strengthen their market positions as standards develop across the sector.

Scope & Segmentation of the Processed and Frozen Vegetables Market

Vegetable Types: Includes broccoli, carrots, peas, spinach, and a wide array of other vegetables that diversify offerings for retail, foodservice, and specialized outlets.

Processing Forms: Encompasses blocks, diced, florets, individually quick frozen (IQF), cubes, sticks, and strips to ensure product flexibility and consistent quality for multiple buyer types.

Distribution Channels: Features convenience stores, specialty retailers, supermarket hypermarkets, and online platforms, each shaping distinct purchasing behaviors and regional approaches.

Source Categories: Covers both conventional and organic solutions that enhance supply chain adaptation and support branding within global markets.

End-Use Applications: Targets food processing, commercial foodservice, and home consumption, guiding supplier relationships and procurement strategies for each use case.

Packaging Formats: Incorporates cartons, clamshell trays, plastic bags, and stand-up pouches to extend shelf life and optimize transportation efficiency.

Regional Analysis: Explores the Americas, Europe, Middle East and Africa, and Asia-Pacific, offering detailed perspectives for the United States, Brazil, Germany, UAE, and China to meet specific market needs.

Leading Companies: Analyzes Conagra Brands, McCain Foods, Bonduelle, Greenyard, Nomad Foods, Fresh Del Monte, Lamb Weston Holdings, Ajinomoto, Royal Cosun, and Ardo, focusing on their strategic initiatives and market leadership.

Key Takeaways for Senior Executives

Increased adoption of automation and machine learning is enhancing supply chain agility, helping companies quickly adjust to shifting customer requirements and anticipate operational demands.

Continuous improvements in health and sustainability are driving new processing techniques, ensuring clearer labeling and ongoing adherence to robust ethical standards.

Sustainable sourcing and responsible resource management are building trust with business partners and clients, advancing compliance, and supporting reliable supply chains.

Decentralized operations improve organizations’ responsiveness to market changes and help preserve business continuity when facing region-specific regulatory or supply challenges.

Diversified sourcing and distribution methods mitigate risk, increasing resilience against rapid shifts in the regulatory or market environment across global business operations.

Why This Report Matters

Enables executive teams to benchmark procurement and risk management strategies in line with present-day market realities by harnessing well-researched industry insights.

Clarifies the influence of digital technology and automation on compliance and efficiency, equipping leadership to manage complex regulatory challenges proactively.

Empowers decision-makers to respond strategically to shifts in regulations, logistics, and sourcing, ensuring steady market positioning.

Conclusion

This report offers strategic, actionable insights to equip senior leaders for responsible growth, operational alignment, and effective navigation within the evolving processed and frozen vegetables market.

Key Attributes:

Report Attribute

Details

No. of Pages

184

Forecast Period

2025 – 2032

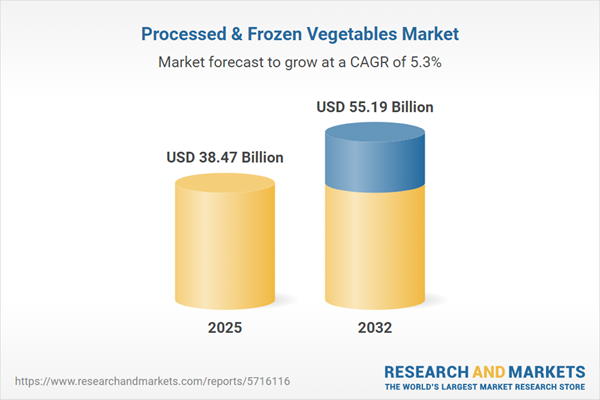

Estimated Market Value (USD) in 2025

$38.47 Billion

Forecasted Market Value (USD) by 2032

$55.19 Billion

Compound Annual Growth Rate

5.2%

Regions Covered

Global

Key Topics Covered:

1. Preface 1.1. Objectives of the Study 1.2. Market Segmentation & Coverage 1.3. Years Considered for the Study 1.4. Currency & Pricing 1.5. Language 1.6. Stakeholders

2. Research Methodology

3. Executive Summary

4. Market Overview

5. Market Insights 5.1. Increasing adoption of sustainable packaging solutions to reduce plastic waste in frozen vegetable distribution 5.2. Integration of advanced freezing technologies to preserve nutrient content and improve product quality 5.3. Growth of convenience-driven single-serve frozen vegetable snack packs for on-the-go consumers 5.4. Expansion of plant-based meal kits featuring pre-cut frozen vegetables to cater to health-conscious households 5.5. Surge in demand for ethnic and specialty frozen vegetable blends reflecting diverse culinary preferences 5.6. Emergence of e-commerce platforms enabling direct-to-consumer sales of frozen vegetables with customizable portion sizes

6. Cumulative Impact of United States Tariffs 2025

7. Cumulative Impact of Artificial Intelligence 2025

8. Processed & Frozen Vegetables Market, by Vegetable Type 8.1. Broccoli 8.2. Carrot 8.3. Pea 8.4. Spinach

12. Processed & Frozen Vegetables Market, by End User Application 12.1. Food Processing 12.2. Food Service 12.3. Household Use

13. Processed & Frozen Vegetables Market, by Packaging Type 13.1. Carton 13.2. Clamshell Tray 13.3. Plastic Bag 13.4. Stand Up Pouch

14. Processed & Frozen Vegetables Market, by Region 14.1. Americas 14.1.1. North America 14.1.2. Latin America 14.2. Europe, Middle East & Africa 14.2.1. Europe 14.2.2. Middle East 14.2.3. Africa 14.3. Asia-Pacific

15. Processed & Frozen Vegetables Market, by Group 15.1. ASEAN 15.2. GCC 15.3. European Union 15.4. BRICS 15.5. G7 15.6. NATO

16. Processed & Frozen Vegetables Market, by Country 16.1. United States 16.2. Canada 16.3. Mexico 16.4. Brazil 16.5. United Kingdom 16.6. Germany 16.7. France 16.8. Russia 16.9. Italy 16.10. Spain 16.11. China 16.12. India 16.13. Japan 16.14. Australia 16.15. South Korea

17. Competitive Landscape 17.1. Market Share Analysis, 2024 17.2. FPNV Positioning Matrix, 2024 17.3. Competitive Analysis 17.3.1. Conagra Brands, Inc. 17.3.2. McCain Foods Limited 17.3.3. Bonduelle S.A. 17.3.4. Greenyard N.V. 17.3.5. Nomad Foods Limited 17.3.6. Fresh Del Monte Produce Inc. 17.3.7. Lamb Weston Holdings, Inc. 17.3.8. Ajinomoto Co., Inc. 17.3.9. Royal Cosun N.V. 17.3.10. Ardo NV

About ResearchAndMarkets.com ResearchAndMarkets.com is the world’s leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood,Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./ CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900

Join millions of self-starters in getting business resources, tips, and inspiring stories in your inbox.

Unsubscribe anytime. By entering your email, you agree to receive marketing emails from BigBCC. By proceeding, you agree to the Terms and Conditions and Privacy Policy.

SELL ANYWHERE WITH BigBCC

Learn on the go. Try BigBCC for free, and explore all the tools you need to start, run, and grow your business.